The Warehousing Gap Squeezing America’s Small Businesses

This analysis draws from 2024-2025 reports from leading commercial real estate firms, including CBRE, JLL, Cushman & Wakefield, and Colliers, supplemented by data from the U.S. Small Business Administration and specialized industrial market researchers.

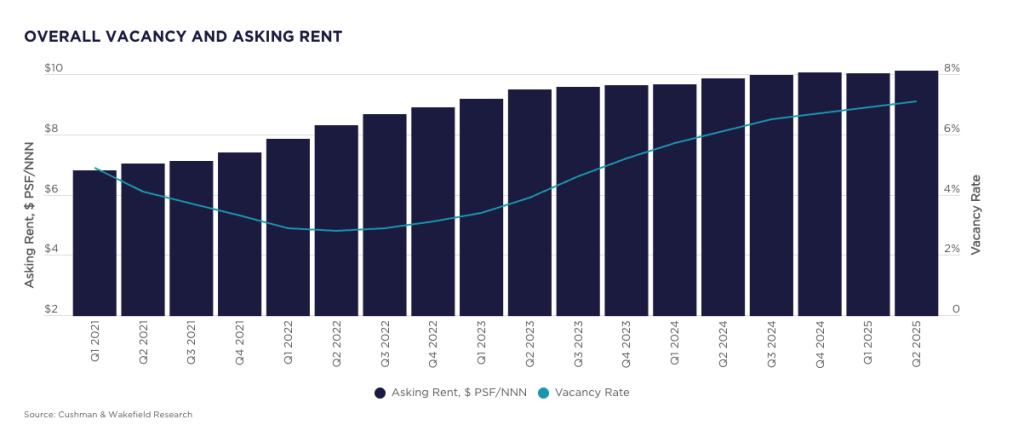

According to Cushman & Wakefield’s latest industrial report, the United States faces a critical shortage of small-format warehouse spaces. The vacancy rate for facilities under 100,000 square feet is just 4.1% compared to over 10% for big-box warehouses. This “missing middle” in industrial real estate has created unprecedented challenges for America’s 34.8 million small businesses, which generate $13.3 trillion annually and employ nearly half the nation’s workforce.

The supply-demand imbalance has pushed small-bay warehouse rents to $12-15 per square foot—a 31% premium over larger spaces (PW Development, 2025)—while new construction remains almost exclusively on mega-facilities averaging 180,000 square feet or more.

Markets Where Small Businesses Struggle Most

PW Development’s 2025 Small-Bay Industrial Report identifies Las Vegas as ground zero for the crisis, with small-bay vacancy rates at just 2.7%—so severe that new projects reach full occupancy within one month of delivery. Atlanta presents a stark dichotomy: while overall industrial vacancy climbed to 10% due to big-box oversupply, small-bay spaces under 50,000 square feet maintain just 4.1% vacancy, with 87% of all lease deals in early 2024 concentrated in this smaller segment.

In Denver, record-high asking rents have forced small business owners to increasingly purchase rather than lease, while Chicago has resorted to converting 3.9 million square feet of office space to industrial use—the most in the nation—to address the shortage.

The crisis extends across all major logistics hubs. Cushman & Wakefield reports that Los Angeles has seen available space increase 61% since 2022, but primarily in large-format facilities that small businesses cannot afford or utilize. Dallas-Fort Worth shows how even markets actively building new supply still face shortages, with small-bay availability at 6.1% despite overall industrial vacancy reaching 9-10% (CommercialSearch, 2025).

Phoenix exemplifies the construction mismatch perfectly: 58.8 million square feet of big-box warehouse under development while small businesses scramble for the few available smaller spaces. From Boston’s infill location shortages to Miami’s acute small industrial scarcity, virtually every major metropolitan area faces this structural imbalance.

Major Real Estate Firms Acknowledge the Gap

CBRE’s 2024 North America Industrial Big-Box Review explicitly defines the problem: while their focus remains on “big-box industrial” facilities of 200,000+ square feet, they recognize growing demand for “small-bay distribution centers” with spaces ranging from 2,250-10,000 square feet. Their data shows construction costs for modern distribution facilities have grown at 2.5 times the general inflation rate since 2019, making smaller facilities economically unfeasible for most developers. Meanwhile, 41% of big-box transactions are dominated by third-party logistics providers, effectively crowding out smaller operators from the market.

JLL has pioneered research on “urban infill warehouse and distribution space” to address last-mile delivery needs, finding that availability in optimal urban locations is 180 basis points lower than the general market. Their research highlights creative solutions like converting Chicago’s Millennium Park parking garages for last-mile fulfillment, but acknowledges these efforts barely scratch the surface of demand.

According to Cushman & Wakefield’s Q3 2024 data, 75% of industrial occupiers have delayed leasing decisions by three or more months, reflecting market uncertainty and limited options for smaller tenants seeking right-sized spaces.

Colliers’ mid-2024 analysis reveals the competitive disadvantage small businesses face: while big-box vacancy rates rose to 10.3%, Asian-based third-party logistics companies now control 27% of that segment, with resources to secure prime locations and negotiate favorable terms that small businesses cannot match. Across all major firms, the consensus is clear—the industrial real estate market has evolved to serve mega-tenants while leaving a significant gap for businesses needing 10,000-50,000 square feet of space.

Hidden Costs Compound the Pricing Crisis

Beyond headline rents, small businesses face a labyrinth of hidden costs that can add $20,000 or more annually to occupancy expenses. Prologis research shows traditional triple net leases require tenants to pay base rent plus fluctuating charges for common area maintenance, utilities that can spike by $2,000 monthly during peak seasons, and insurance requirements that landlords mandate with little flexibility.

The complexity has intensified: 46.67% of warehouses now impose monthly minimums that surged from $195 in 2023 to $337.50 in 2024, with projections reaching $517 by 2025, according to the Warehousing and Fulfillment Cost Survey.

The pricing transparency crisis hits small businesses particularly hard. McKinsey research shows 60% of companies with fewer than 25 employees will switch providers in response to any price increase, yet most lack the negotiating power to secure better terms. While enterprise clients negotiate volume discounts and custom agreements, small businesses face standardized contracts with early termination penalties often equal to several months of rent.

New long-term storage fees have emerged at 48.6% of warehouses in 2025, adding $5-10 per pallet monthly for slow-moving inventory—a cost structure that disproportionately impacts smaller operations with less predictable turnover.

The disparity extends to lease flexibility. While 56.67% of warehouses now offer month-to-month terms (Warehousing and Fulfillment, 2024), these typically come with premium pricing that small businesses struggle to afford. Traditional leases requiring 3-10 year commitments create adaptability challenges for growing companies, yet shorter terms often mean higher rates. Emerging solutions like all-inclusive pricing models from providers such as Prologis’ “Clear Lease” program offer hope, but adoption remains limited and often restricted to larger markets where small businesses already face the highest competition.

Operators Struggle to Connect with Growing Small Business Demand

The disconnect between warehouse operators and small businesses represents a massive missed opportunity. America’s small businesses have filed 5.5 million new applications since 2023, with e-commerce adoption driving exponential growth in warehouse demand—online retailers require 1.2 million square feet of warehouse space per million dollars in sales, three times more than traditional retail (CrowdStreet, 2024). Yet 73% of these businesses lack confidence in their marketing strategies and dedicate less than one hour daily to marketing activities, making them nearly invisible to traditional warehouse marketing approaches.

Operational challenges compound the connection problem. BKM Capital Partners, managing small-bay properties, processes over 600 leases annually with a staff of 100—highlighting the operational intensity of serving smaller tenants. While small-bay warehouse sales volume runs 32% above pre-COVID levels (Plante Moran, Q2 2025) and these tenants typically pay rent more reliably than large corporations, many operators lack the systems and processes to efficiently manage multi-tenant facilities. The result is a market where small-bay spaces maintain just 4% vacancy rates while operators struggle to identify and reach potential tenants.

The technology gap further widens the divide. Small businesses increasingly demand turnkey solutions with integrated logistics software, yet most warehouse operators provide only basic storage. With 59% of small businesses now incorporating AI into their operations and expecting omnichannel capabilities as table stakes, the traditional warehouse model fails to meet their evolving needs. This mismatch occurs even as transportation and warehousing sectors project adding 387,000 new jobs through 2033 (CBRE, 2024), with the logistics market expected to grow at 7.2% annually through 2030.

The Path Forward

The “missing middle” in warehouse space represents both a critical challenge and an unprecedented opportunity in American commercial real estate. With small businesses contributing 43.5% of GDP yet facing vacancy rates below 5% for appropriately sized facilities, the market failure is clear and quantifiable. The solution requires more than incremental adjustments—it demands new models that bridge the gap between big-box logistics and small business needs, combining transparent pricing, flexible terms, and technology-enabled services that allow America’s entrepreneurial engine to compete effectively in an increasingly digital economy.

The data reveals that markets addressing this gap through innovative approaches—from co-warehousing models to all-inclusive pricing structures—are capturing significant value while supporting small business growth. As construction costs make sub-75,000 square foot developments economically challenging under traditional models, the opportunity lies in reimagining how small-format industrial space is developed, marketed, and managed.

For platforms like WareCRE that connect small businesses with flexible, transparently priced warehouse solutions, the market conditions have never been more favorable for disrupting an industry that has left millions of businesses underserved.

Sources

Industry Reports:

- Cushman & Wakefield – U.S. Industrial MarketBeat Report (Q3 2024)

- CBRE – 2024 North America Industrial Big-Box Review & Outlook

- JLL – United States Industrial Market Dynamics (Q4 2024)

- Colliers – Midyear 2024 Industrial Report

- PW Development – Small-Bay Industrial 2025 Trend Report

Government Data:

- U.S. Small Business Administration – Frequently Asked Questions About Small Business (2024)

- SBA Office of Advocacy – Small Business Report (November 2024)

Market Analysis: